Earlier this week, the HHS released a report (pdf) on Obamacare premiums. Yglesias, who posts the above chart, observes that the “average subsidy-eligible enrollee in the federal exchange gets a pretty cheap health plan.” But that fact worries Bob Laszewski:

The lowest income people––who pay the lowest premiums and out-of-pocket costs––are the ones who are obviously signing up. That explains why the average consumer subsidy is so high and the average net cost is so low.

As I have said on this blog before, the biggest consumer problem Obamacare has is that the plans––with their still high premiums even after the subsidy, big deductibles, and narrow networks––are not attractive to working class and middleclass families and individuals.

Simply, the Obamacare plans are unattractive to all but the poorest who get the biggest subsidies and the lowest deductibles.

Suderman points out that the “data released by the administration doesn’t account for premiums in the 14 states that ran their own exchanges this year” and that “those averages conceal an awful lot of variation.” He goes on to cite a Manhattan Institute study finding that health insurance has gotten significantly more expensive under Obamacare:

[T]he study by health policy fellow Yevgeniy Feyman found that, on average, premiums were up 49 percent under Obamacare. Again, that’s an average, and it masks some variation—in New York, which had unusually restrictive, badly designed health insurance market rules prior to Obamacare, premiums are actually down quite a bit—but it indicates that the overall trend for unsubsidized premiums is up.

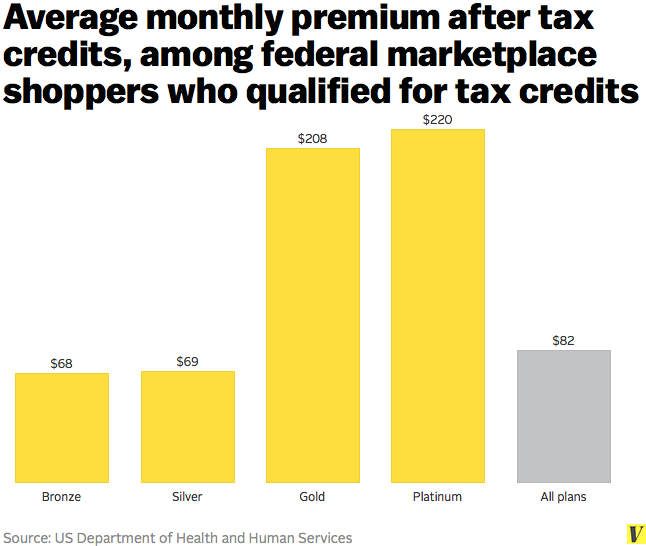

The difference, then, is being made up by federal subsidies. According to the administration’s report, those subsidies are carrying 76 percent of the total cost of subsidized insurance plans selected in the federal exchange. The out-of-pocket average is $82. But the actual average premium price, without subsidies, is $346.

But the exact size of those premium increases is up for debate:

[A] new analysis from a conservative health-care economist suggests that Obamacare sticker shock wasn’t nearly as steep as other studies previously suggested. Consumers who bought their own coverage between 2010 and 2012 saw the average cost of their plan increase between 14 percent and 28 percent when they switched to new coverage under the Affordable Care Act, according to Mark Pauly, a professor of health-care management at the University of Pennsylvania’s Wharton School of Business.

Adrianna McIntyre digs into the details of that study. Why costs went up:

On balance, the authors suggest that the hike is attributable to insurers expecting an influx of sicker enrollees. Health reform makes insurance easier to obtain for sick people. The new insurance rules means that cost gets spread around across the sick and the healthy, so when enrollees get sicker overall, prices go up for everyone.

The other factor that might have driven up prices — the essential benefits package — doesn’t seem to have played a major role. This new paper finds that the generosity of the insurance benefits offered before Obamacare was roughly similar, on average, to the medium-level plans on today’s exchanges. And that suggests the change in who’s enrolling in insurance — not the richness of those insurance benefits — is driving the rise in prices.