Chad Stone was disappointed by the GDP report:

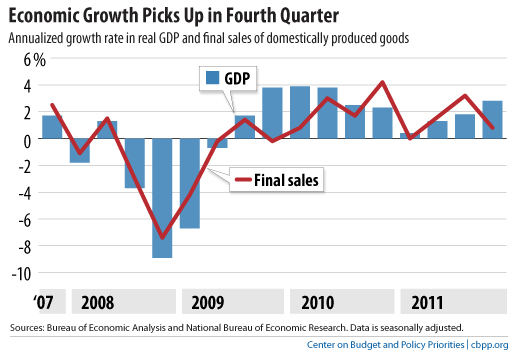

Critically, the jump during the third quarter in final sales of goods and services— a better measure of underlying demand than GDP —didn’t continue in the fourth quarter … [see chart above] . More than half of the growth in GDP in the fourth quarter came from inventory accumulation — that is, unsold goods piling up on the shelves.

Karl Smith counters:

There is … a bit of handwringing over the fact that inventories contributed so much to GDP growth. But, what does this tell you. Most of this is autos. During the summer there was a major slowdown in parts from Japan. So Hondas and Toyotas started getting lean on lots. Now, they are coming back. That’s inventory adjustment. But, it tells us little about the underlying economy.

Yglesias thinks this kind of growth isn't enough:

GDP grew at a 2.8 percent annualized rate in the fourth quarter, up from 1.8 percent in the third quarter. That's a perfectly respectable number for an economy at full employment to put up, but it's not the kind of "catch-up" growth rate that gives you recovery from a recession.

Scott Hoyt warns:

It is clearly premature to conclude that the economy is off and running. The outlook appeared to be improving at this time last year, only to be derailed by an unexpected surge in commodity prices and fallout from the Japanese earthquake. It would not take much to repeat the pattern this year, since business and consumer sentiment remains brittle from the effects of the Great Recession and events in Washington.

Mark Thoma blames austerity:

[P]remature austerity — cutting spending before the economy is ready for it — is taking a toll on the recovery. The fall in government spending reduced fourth quarter growth by .93 percent — if government spending had remained constant GDP growth would have been 3.7 percent rather than 2.8 percent. This is the opposite of what the government should be doing to support the recovery. We need a temporary increase in government spending to increase demand and employment through, for example, building infrastructure. That would help to get us out of the deep hole we are in, but instead the government seems to be trying to make it harder to escape.

Brad Plumer reminds everyone that these numbers aren't set in stone:

The current GDP numbers are just a first-pass estimate. These numbers will get revised at least twice in the months ahead. Sometimes they get revised very significantly (for instance, it took three years for the Bureau of Economic Analysis to figure out that the recession in the winter of 2008-2009 was much, much, much worse than anyone knew).

And Jared Bernstein hopes the economy increases its momentum:

[H]ave we hit escape velocity from the clutches of the Great Recession? I’d say no, not yet. We’re headed in the right direction, we’ve got some mo, but growth is too slow and there’s still too much fragility and slack in the system.

{kind=link}