Greece issued its first new bonds since its restructuring this morning, raising 3 billion euros. Mark Gilbert, however, discourages celebration:

The front page of today’s Financial Times newspaper heralds today’s sale as Greece coming “out of bond exile,” and describes it as “a sign of growing confidence in the region’s weakest economies.” I beg to differ. First, the sale is evidence that yield-starved bondholders staring at record-low returns on even Italian and Spanish debt holdings are growing more desperate with every lurch lower in bond rates. Second, it shows that investor faith in European Central Bank President Mario Draghi’s pledge to do “whatever it takes” to secure the future of the euro remains unshaken, even though that July 2012 promise has never been tested.

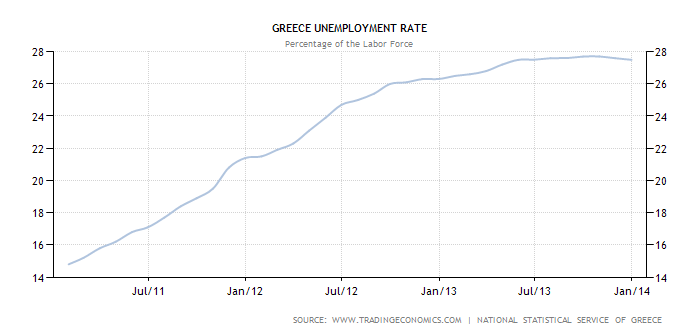

Pointing to the chart above, Ryan Cooper thinks it’s very premature to talk about a recovery:

Indeed, I rather fear this could be the worst of all worlds.

Moving off the Euro would have been awful, but at least held the prospect of returning to growth and full employment within a couple years (from a much lower base). By contrast, the bank Natixis recently estimated that, given very generous assumptions, it will take Spain (which is in similarly dire straits) 25 years to return to 2007-era employment. A nation can do a great deal of catch-up growth in that time.

Realistically, I’d guess this means that Spain, Greece, Italy, Portugal, Ireland, etc., will never recover fully, and instead we’re witnessing the birth of a crummy, tattered Franco-German empire with a permanently depressed periphery.

Sam Ro describes just how crippling the country’s unemployment rate still is:

According to new data from the Hellenic Statistical Authority, Greece’s unemployment was at a staggering 26.7% in January. This is up from 26.5% a year ago, but down from 27.2% in December. In January 2009, the unemployment rate was at 8.9%. The economic crisis has been particularly harsh for young workers. The unemployment rate among 15-24-year-olds and 25-34-year-olds were at 56.8% and 35.5%, respectively.