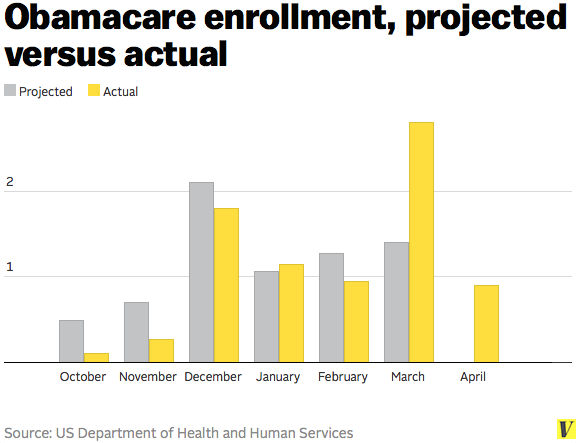

German Lopez charts the Obamacare open enrollment tally (pdf) released yesterday:

Health and Human Services found that, of the 5.2 million people required to answer a question about whether they had insurance at time of signing up, 13 percent (695,000 people) said they already had coverage. That suggests a high proportion of people seeking coverage on the exchanges weren’t replacing an old plan, and, instead, they were without health insurance when they signed up. (The White House, however, cautioned that this data is unreliable.)

This would be a much higher proportion of newly-insured enrollees on the exchange than other analyses have suggested.

Drum was surprised by this welcome news:

In other words, in total, the exchanges signed up about 6.5 million people who were previously uninsured. This is far, far higher than previous estimates of about 3 million or so. I’m not sure what to make of this given the amount of survey data that produced the smaller figure. Perhaps it’s a difference in what counts as uninsured? Or a difference in how people respond to pollsters vs. how they respond to an official question on an application. Hard to say. The full HHS report is here, and it acknowledges the different estimates but provides no guesses about why they vary so widely.

For now, just take this as a bit of a mystery. In a month or two we’ll probably have much firmer data on all this stuff.

Suderman digs into the numbers:

[I]t’s still not clear how many of these sign-ups have actually paid—or will pay—their first month’s premium, and are therefore completely enrolled in coverage. Not that this uncertainty is hampering the administration’s boasts. On Twitter, HHS Secretary Sebelius has posted HealthCare.gov-branded graphics saying that 8 million are enrolled through the exchanges. Sebelius should read her own agency’s report. It states quite clearly that “it is important to note that the Marketplace plan selection data as of the end of the open enrollment period do not represent effectuated enrollment (e.g., those who have paid their premium).”

Cohn examines the demographic breakdowns:

According to HHS, 28 percent of people selecting private plans are between the ages of 18 and 34. That’s almost exactly the same as it was inMassachusetts, when that state introduced its version of the same reforms.

But there isn’t one, unified national insurance market. There are 51 separate markets, for the states and the District of Columbia, and the numbers vary a lot from market to market. Some states, including several in the Deep South, have even higher precentages of young adults between 18 and 34. (The District has by far the most, with 45 percent, but that’s for idiosyncratic reasons.) But in other states it’s much, much lower—18 percent in West Virginia, for example, and 22 percent in Ohio.

Insurers in those states might end up raising rates significantly next year, although it will depend on a bunch of other factors, like what kind of enrollment insurers were expecting.

Kliff zooms out:

Kaiser Family Foundation estimates 28 million people without coverage were eligible to buy coverage on the exchanges. About a quarter of them decided to. That still leaves another 20 million people who didn’t purchase insurance – maybe because they didn’t want to, or were confused, or never even heard there were options to begin with.

“CBO has enrollment ramping up next year to 13 million and that feels like a pretty big leap given how hard it was to hit 8 million,” says [Kaiser Family Foundation’s Larry] Levitt. The people who signed up in 2014 were likely the most motivated, the low hanging fruit for enrollment workers. The people who will be pitched in 2015 sat out the first round of sign-ups and, come next year, could be a tougher sell.