Last Friday, Chris Giles alleged on the pages of the Financial Times that Thomas Piketty’s Capital in the 21st Century contains major data errors that undermine his entire theory. Jordan Weissmann outlines Giles’ accusations:

First, it says Piketty has covered up a giant gap in America’s historical records on wealth concentration. “There is simply no data between 1870 and 1960,” the newspaper states. “Yet, Prof. Piketty chooses to derive a trend.” This charge is neutered a bit by the fact that Gabriel Zucman and Emmanuel Saez recently released a detailed analysis of U.S. wealth inequality dating back to 1913 that shows an even more dramatic increase than what Piketty found. But Piketty will nonetheless need to spell out how he reached his own conclusions in a bit more detail.

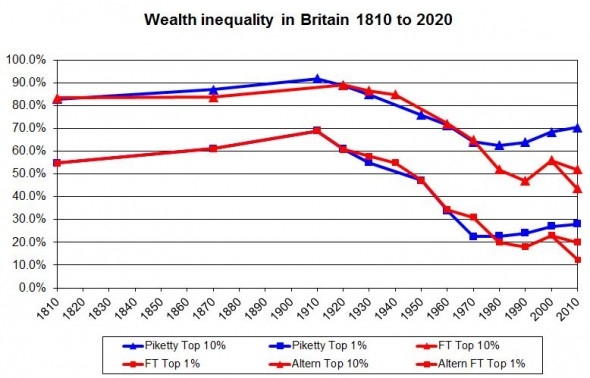

The much more important point of contention is Great Britain. The FT argues that Piketty’s graphs simply “do not match” his underlying data on the UK, and that official estimates show no significant increase in the country’s concentration of wealth since the 1970s. Once Britain’s corrected data is included in the picture, the FT argues, the evidence that wealth inequality is growing across Europe disappears.

“But,” Tim Fernholz interjects, “it’s not clear that Piketty’s analysis is entirely doomed”:

Giles says that he has refuted two of Piketty’s notions: That wealth inequality has begun to increase in the last 30 years, and that the US has a more unequal distribution than Europe. But Giles’ final chart, comparing US and European inequality, is ambiguous on this score. The chart is a mix of different datasets, some of which show wealth inequality appearing to increase—albeit so slightly that it might be a statistical error—after 1980. And some show that US inequality is higher than in Europe—even without including the Saez-Zucman data [here], where the effect is more pronounced …By that reading, Piketty’s ideas could still be plausible, even though problems need to be rectified and further work is needed. No doubt many eager economics grad students are licking their chops.

Krugman is incredulous over Giles’ contention that there is “no obvious upward trend” in inequality:

I don’t know the European evidence too well, but the notion of stable wealth concentration in the United States is at odds with many sources of evidence. Take, for example, the landmark CBO study on the distribution of income; it shows the distribution of income by type, and capital income has become much more concentrated over time:

It’s just not plausible that this increase in the concentration of income from capital doesn’t reflect a more or less comparable increase in the concentration of capital itself. Beyond that, we have, as Piketty stresses, evidence from Forbes-type surveys, which show soaring wealth at the very top. And we have other estimates of wealth concentration, like Saez-Zucman, that use completely different methods but point to the same conclusion.

“Even if you believe that Giles’s findings dramatically change Piketty’s results,” Danny Vinik argues, “they have little bearing on his economic theory”:

Giles makes a passing comparison to economists Carmen Reinhart and Ken Rogoff (R&R), who drove a significant part of Republican austerity agenda, but saw their findings disproven in 2013. Liberals celebrated when Thomas Herndon, a graduate student from UMass Amherst, discovered a spreadsheet error in R&R’s results that invalidated their main finding. But unlike Piketty, Reinhart and Rogoff largely had no economic theory to ground their argument that national debt crises occur when a country’s debt level surpasses 90 percent of GDP. Once their data fell apart, their theory had no legs to stand on. On the other hand, Piketty fits data to this theory, but does not depend on it. Piketty’s theory—right or wrong—is largely unaffected by these results.

Ryan Avent makes a similar point:

First, the book rests on much more than wealth-inequality figures. Second, the differences in the wealth-inequality figures are, with the exception of Britain, too minor to alter the picture. And third, as Mr Piketty notes in his response, Chapter 10 is not the only analysis of wealth inequality out there, and forthcoming work by other economists (some conclusions of which can be seen here) suggests that Mr Piketty’s figures actually understate the true extent of growth in the concentration of wealth.

Mike Konczal piles on, saying Giles misconstrues Piketty’s argument:

[R]ising inequality in the ownership of capital is not the necessary, major driver of the worries of the book. It isn’t that the 1% will own a larger share of capital going forward. It’s that the size and importance of capital is going to go big. If the 1% own a consistent amount of the capital stock, they have more income and power as the size of the capital stock increases relative to the economy, and as it takes home a larger slice. However, obviously, if inequality in wealth ownership goes up, it will make the situation worse. (It’s noteworthy that these numbers Giles is analyzing aren’t introduced until Chapter 10, after Piketty has gone through the growth of capital stock and the returns to capital at length in previous chapters.)

The way that Giles could put a serious dent into Piketty’s theory through this analysis is by showing that inequality of wealth ownership is falling in the recent past. This is not what Giles finds. He mostly finds what Piketty finds, except in England, where it’s flat instead of slightly growing in the recent past.

But Cowen takes the data problems seriously:

Now, when you cut through the small stuff, the new empirical problem seems to be that UK revisions, combined with a population-weighted series for Europe, contradicts Piketty’s claim of rising wealth inequality for Europe. I would call that a serious problem. I am not impressed by the “downplaying” responses which focus on coding errors, Swedish data points, and the other small stuff. Let’s face up to the real (new) problem, namely that robustness suddenly seems much weaker.

In any case, Patrick Brennan believes that Piketty never made a convincing case for his general thesis:

Piketty set out to do something much more audacious than prove that income inequality is rising in the United States and in most wealthy countries — that’s relatively easy to prove, even if the increase has been substantially overstated. Rather, he wanted to show that this plays into a loop with increasing wealth that needs to be arrested by huge global interventions. One common objection to Giles’s skepticism tonight has been that increasing wealth inequality is simply an obvious fact of this world — why do we need the data to back it up? Well, Piketty needs the data to back up the arguments he made with it — he needs wealth inequality not just to appear high or to be rising, but to be returning to 19th-century levels as a matter of economic inevitability. The errors he made may not be devastating to the work he’s done to prove this so far, but even without taking them into account, he hasn’t yet justified his dramatic conclusions.

Lastly, noting that data errors are a fact of life in the social sciences, Nate Silver encourages skepticism of both Piketty’s argument and Giles’ critique:

The closest thing to a solution is to remain appropriately skeptical, perhaps especially when the research finding is agreeable to you. A lot of apparently damning critiques prove to be less so when you assume from the start that data analysis and empirical research, like other forms of intellectual endeavor, are not free from human error. Nonetheless, once the dust settles, it seems likely that both Piketty and Giles will have moved us toward an improved understanding of wealth inequality and its implications.

Previous Dish on Capital here.

{kind=link}