Amazing but true. I really want to support Rand Paul. It gets harder all the time.

Month: May 2014

Rights-Based Development?

Brian Doherty praises William Easterly’s Tyranny of Experts for how it tackles the follies of the international development industry:

Easterly is particularly sharp on the looseness of much of the “data” that development experts rely on. He mocks Bill Gates, the Uncle Pennybags of modern development econ, for crowing about a five-year improvement in Ethiopian child mortality rates. Easterly convincingly describes a confusing data landscape, marred by lack of well-kept vital records in shoddy states, and wildly varying estimates from different independent sources doing the best they can with the bad source material they have to deal with. In fact, we have no way to get an accurate picture about infant and child death in the Third World. Our macro data on the economies of the poorer parts of the world are too unreliable and inconsistent to use as much of a measure of anything.

But he sees flaws with the book:

[F]or a book trying to make the case that poor, autocratic governments harm their citizens’ rights with the connivance of western development experts, Tyranny of Experts lacks sufficient specifics of how and why that is so, or enough vivid stories demonstrating the specific human costs of development hubris. It’s almost as if Easterly thinks his claims are so obviously true that he doesn’t have to get bogged down in the details of proving them.

The Economist is not so sure about Easterly’s big-picture ideas:

Mr Easterly is at his trenchant best when demolishing various bits of received wisdom about development, whether about the role of strong leaders or the idea that policymakers actually know how to choose the right policies. Often they do not; nor do economists. This makes it harder to share his confidence that securing individual rights will do the trick. Rights clearly matter, but there is also a lot of evidence that individuals, like policymakers, do not make efficient use of all the information available. Instead they often rely on quick, flawed rules of thumb to guide their decisions. Securing rights may be necessary, but it is unlikely to be sufficient.

Mr Easterly claims that the “difference between individualist and collectivist values” is one of the great divides that explains why Western Europe prospered in the early modern age as the rest of the old world fell behind. True, Westerners today stress things like self-reliance, where East Asians might value group loyalty. Yet history surely matters here.

Eric Posner came to similar conclusions in a review he wrote last month:

Which rights should we advocate? How should we insist that they be implemented? What should we do to governments that refuse to take our advice? I suspect that if he gave these questions some thought, he would realize that any serious effort to compel or bribe poor countries to recognize rights would look like the development activities that he criticizes. Indeed, his bête noir, the World Bank, famously tried to implement “rule of law” projects that were supposed to enhance rights. These projects failed for all the reasons that all the other development projects failed.

In March, the Dish highlighted an excerpt from Easterly’s book.

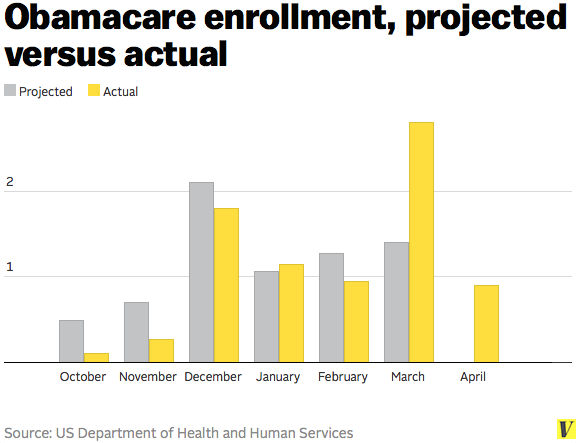

The Dust Starts To Settle On Enrollment

German Lopez charts the Obamacare open enrollment tally (pdf) released yesterday:

Health and Human Services found that, of the 5.2 million people required to answer a question about whether they had insurance at time of signing up, 13 percent (695,000 people) said they already had coverage. That suggests a high proportion of people seeking coverage on the exchanges weren’t replacing an old plan, and, instead, they were without health insurance when they signed up. (The White House, however, cautioned that this data is unreliable.)

This would be a much higher proportion of newly-insured enrollees on the exchange than other analyses have suggested.

Drum was surprised by this welcome news:

In other words, in total, the exchanges signed up about 6.5 million people who were previously uninsured. This is far, far higher than previous estimates of about 3 million or so. I’m not sure what to make of this given the amount of survey data that produced the smaller figure. Perhaps it’s a difference in what counts as uninsured? Or a difference in how people respond to pollsters vs. how they respond to an official question on an application. Hard to say. The full HHS report is here, and it acknowledges the different estimates but provides no guesses about why they vary so widely.

For now, just take this as a bit of a mystery. In a month or two we’ll probably have much firmer data on all this stuff.

Suderman digs into the numbers:

[I]t’s still not clear how many of these sign-ups have actually paid—or will pay—their first month’s premium, and are therefore completely enrolled in coverage. Not that this uncertainty is hampering the administration’s boasts. On Twitter, HHS Secretary Sebelius has posted HealthCare.gov-branded graphics saying that 8 million are enrolled through the exchanges. Sebelius should read her own agency’s report. It states quite clearly that “it is important to note that the Marketplace plan selection data as of the end of the open enrollment period do not represent effectuated enrollment (e.g., those who have paid their premium).”

Cohn examines the demographic breakdowns:

According to HHS, 28 percent of people selecting private plans are between the ages of 18 and 34. That’s almost exactly the same as it was inMassachusetts, when that state introduced its version of the same reforms.

But there isn’t one, unified national insurance market. There are 51 separate markets, for the states and the District of Columbia, and the numbers vary a lot from market to market. Some states, including several in the Deep South, have even higher precentages of young adults between 18 and 34. (The District has by far the most, with 45 percent, but that’s for idiosyncratic reasons.) But in other states it’s much, much lower—18 percent in West Virginia, for example, and 22 percent in Ohio.

Insurers in those states might end up raising rates significantly next year, although it will depend on a bunch of other factors, like what kind of enrollment insurers were expecting.

Kliff zooms out:

Kaiser Family Foundation estimates 28 million people without coverage were eligible to buy coverage on the exchanges. About a quarter of them decided to. That still leaves another 20 million people who didn’t purchase insurance – maybe because they didn’t want to, or were confused, or never even heard there were options to begin with.

“CBO has enrollment ramping up next year to 13 million and that feels like a pretty big leap given how hard it was to hit 8 million,” says [Kaiser Family Foundation’s Larry] Levitt. The people who signed up in 2014 were likely the most motivated, the low hanging fruit for enrollment workers. The people who will be pitched in 2015 sat out the first round of sign-ups and, come next year, could be a tougher sell.

Floating Nuclear Power

It could happen:

There are many things people do not want to be built in their backyard, and nuclear power stations are high on the list. But what if floating reactors could be moored offshore, out of sight? There is plenty of water to keep them cool and the electricity they produce can easily be carried onshore by undersea cables. Moreover, once the nuclear plant has reached the end of its life it can be towed away to be decommissioned. Unusual as it might seem, such an idea is gaining supporters in America and Russia. …

The American researchers think there is no particular limit to the size of a floating nuclear power station and that even a 1,000MW one—the size of some of today’s largest terrestrial nuclear plants—could be built. They believe the floating versions could be designed to meet all regulatory and security requirements, which would include protecting the structure from underwater attack, says Dr [Neil] Todreas.

The View From Your Obamacare: Mental Health

A few readers coalesce around a new theme:

My husband and I are both self-employed and work from home, and for the first time, our entire family has health insurance – thanks to Obamacare. My husband was uninsured for years, because he just couldn’t get health

insurance that wasn’t exorbitant. In 2012, he tried to get health insurance from three different health insurance companies and got turned down from each one for minor health issues. The reason for his last rejection was – I kid you not – “impending fatherhood.” When a health insurance company declared that my pregnancy (which was covered under my insurance) somehow became a pre-existing condition for him, we gave up on the whole Kafka-esque scenario and just waited for 2014.

But I mostly want to highlight another Obamacare benefit that hasn’t been mentioned much: mental health coverage. I have PTSD, which my pre-Obamacare policy didn’t cover. As a result, I could get 10 group or individual therapy sessions per calendar year, and I could see a shrink once every two months for ten minutes for medication management, and that was it. I could never switch policies because no one else would cover me. (Put PTSD on a health insurance application and they couldn’t write the denial letter fast enough.)

I spent $18,000 out of pocket to treat my PTSD (and four years after completing therapy, I’m STILL paying off the resulting credit card debt.) EMDR was worth every damn penny, because while I still have some remaining symptoms, I can actually sleep through the night, I don’t have to manage multiple flashbacks a day, and I’m not crawling out of my skin with anxiety twice a day. I’m grateful that my therapist offered a no-interest payment plan and that I had the resource of a high credit limit, but not having health coverage for my PTSD treatment was a huge financial hit at a time when I was already struggling to get by.

Like a lot of people with a mental illness, I don’t broadcast my PTSD diagnosis – mostly because I don’t necessarily want to discuss my abusive childhood in public. But access to mental health treatment is a big deal for a lot of people like me, and I’m grateful that I have options now that I didn’t have before.

Another also touches on mental illness:

I love this thread, and I thought I’d chime in because the policy has meant a lot to me and my family. My mom is very well employed and well insured. However, prior to Obamacare her coverage only covered her 7 children if they were under 18 or in school full time and under 25. This was without a doubt a luxury plan in comparison to the vast majority of Americans.

Cue disaster 1. My brother had to drop out of college after a suicide attempt and diagnosis of bipolar disorder. He was in inpatient care for weeks, and then seeing multiple doctors to find the right treatment plan to manage the illness. For years.

Now, again, my family was in a relatively secure position prior to this. But the fact that the Obamacare clause for children 26 and under came into effect just six months before this disaster means that my mother didn’t have to make a choice between bankruptcy or leaving one of her children to homelessness or death. Because that’s what the options were pre-Obamacare. And I’d like to point out that no matter how well you raise your kids, no matter how much money you have or how hard you work, you can’t prevent bipolar disorder. You don’t get a choice as an individual to have a mental illness (or cancer, or asthma, or allergies …). How can anyone want to go back to a world where your financial security depends on the luck of the genetic draw?

Once that had (mostly) settled down, we hit disaster 2. My other brother graduated from college, unemployed, and came home to work. He was working three jobs to make ends meet when he got in a motorcycle crash that left him inches from death. He was in the hospital for the better part of a day before they were even able to identify my mother and call her. He woke up two days later and but for the grace of god was not just alive but didn’t lose any brain damage. He spent weeks in inpatient rehab, several more in outpatient rehab, and a year later had the final surgery to fix his hip.

To be clear, my brother was working three jobs and none of them offered insurance. He is the epitome of a the “hard working American.” And once again, if it weren’t for Obamacare, he would have spent decades of his life trying to come back from financial ruin. Or my family would have gone bankrupt.

If there’s anything I learned from my family’s story, it’s the crushing economic impact of not having health insurance. Without that one clause, my family would have gone from gone from solidly upper middle class to near-poverty in a single generation. We would have gone from drivers of the economy – spending money on restaurants, vacations, college, homes – to the paycheck to paycheck existence that too many Americans endure. I am aware of just how lucky we are, and I wish other people who think Obamacare is only the rich subsidizing the lazy poor would realize just how much security and wellbeing Obamacare has brought all Americans.

Read the whole thread here.

(Photo by Yoon S. Byun/The Boston Globe via Getty Images)

Finnegans Headache

Andrew McGarth considers the difficulties of translating Joyce’s byzantine final novel into Chinese:

Dai Congrong started translating the book in 2006, but didn’t publish the first part of her translation until early 2013. Part of the reason it took so long is that Finnegans Wake, while challenging enough to read in English, is even more difficult to translate, owing to James Joyce’s puns, allusions, and multi-layered meanings which baffle most native English speakers and often lose their meaning in translation. The novel has been deemed “untranslatable” and the translations that are successful tend to be consuming: the Polish version took 10 years to finish, the French version 30 years, and the Japanese version took three separate translators after the first disappeared and the second went mad. …

Dai’s translation only covers the first third of the book and clocks in at 775 pages; for comparison, the full English text is 676 pages long. Most of the extra pages can be attributed to footnotes and annotations, which were needed to make sense of the novel. According to the Wall Street Journal, the first sentence of Dai’s translation is accompanied by two definitions, five footnotes, and seven asides that explain the possible intended meanings for the word “riverrun” and the allusions to an 18th century academic named Giovanni Battista Vico, and for later sentences in the book Dai had to create new Chinese characters to capture sounds from the novel. Talking to Reuters after the book’s release, she said she started having doubts early on, when after two years of work she had yet to translate one word.

Relatedly, illustrator Stephen Crowe, who is translating Finnegans Wake into images for his project Wake In Progress, discusses how the book has changed his approach to reading:

Most books develop their themes through the plot and the way the characters change over time. Finnegans Wake uses those techniques to some extent, but mostly [Joyce] uses others. The most important one is probably the leitmotif. He marks out different ideas with certain words, letters, numbers or rhythms, so you can trace the development of each idea according to the way he develops the motif. Like in music. Repetition is what powers the whole thing. But reading the Wake teaches you to read in a Wakean way. After a while, you find yourself reading conventional books with half an ear for all the words they repeat and the images they reuse. After all, any story is basically a collection of themes organized in a certain way. That’s one thing that you can definitely take from reading the Wake: it makes you re-evaluate everything you think about reading and writing.

When Politics Runs In The Family

A well-connected family helps if you want to be in Congress:

Across all Congresses — House and Senate — from 1789 to 1986, nearly nine percent of legislators came from families that had previously sent a member to Congress. The prevalence of these dynastic legislators has decreased over time. “While 11 percent of legislators were dynastic between 1789 and 1858, only 7 percent were dynastic after 1966,” the authors write. And that number has been mostly flat, according to an October 2013 analysis by Chris Wilson of Time, who found that 6.9 percent of current House and Senate members — 37 in total — come from dynastic families.

As for senators, 13.5 percent have come from dynastic families, versus only 7.7 percent of representatives. One of the key findings of the dynasty paper is that political power is self-perpetuating: “Legislators who hold power for longer become more likely to have relatives entering Congress in the future. Thus, in politics, power begets power.”

Aaron Blake notes that ” for everyone who professes to be disgusted with the idea of another Bush or another Clinton inhabiting the White House, there are many more people who are quite fond of the predictability and ease of voting for a name they know”:

Case in point: The new Washington Post-ABC News poll. The poll shows both the Bush and Clinton political dynasties are viewed in quite positive lights, though the Clinton family reigns superior for now. While 64 percent of registered voters have a favorable view of the Clinton family, 56 percent say the same about the Bushes. And in an age in which it’s hard to get a majority of Americans to agree on anything and especially any politician, that level of support is striking.

Amy Davidson is troubled by American support of political dynasties:

We talk so much about the role of money in politics. Why isn’t all that investment yielding us any truly interesting products in the candidacy sector? It is as if our entire political portfolio were put into the same few stocks that had been there forever. Maybe it is money that, perversely or purposefully, stifles political entrepreneurship and innovation; maybe other factors are at work. In either case, the current situation can’t be for the best, if it serves to make politics seem like a deadened realm rather than a place to bring and work out grievances. We are stretched out, paralyzed, in the polls. What hurts the most is that we may be suffering from a national failure of political imagination.

Budding Books

Tania Unsworth considers the joys of “reading like a kid”:

[A]lthough I love books almost more than anything else in the world, there are probably only a handful I have read as an adult that I would say changed my life. And even then – speaking honestly – the changes to my life have been fairly modest. Reading A Room of One’s Own by Virginia Woolf at the age of 22, for example, certainly challenged my way of thinking, but did it do more than that? If I had missed out on Ishiguro’s Never Let Me Go, to take another example, my life would definitely have been the poorer. But would it have really mattered that much?

I know there are plenty of people who will disagree with this, pointing to books that profoundly and demonstrably altered the course of their adult lives, but speaking personally, the books that had the greatest and most lasting impact on me were all read before the age of fifteen. Am I the only one who feels this? … There was an intensity to reading then, a kind of total involvement in story that is hard to reproduce as an adult. I know too much now about tired plots and clichés. I am always comparing one thing to another, recognizing devices, identifying styles. No matter how good or bad I find something, I’m always aware of my response, slightly detached, consciously enjoying or not enjoying. That’s how it should be. I’m an adult after all. But I do sometimes long to read the way I used to.

Trucking Gets A Flat

Lydia DePillis checks in on the industry:

[Miguel] Tigre came to America from Ecuador 30 years ago, started driving for one of the hundreds of small trucking companies that serve the port and, by 1993, had saved enough to buy a truck. It seemed like a fair trade: As an owner-operator working on contract, he gave up some stability in exchange for the freedom of working whenever he wanted.

But then, the bargain broke down. Prices started rising, and Tigre’s pay rate didn’t keep up. Diesel used to be 87 cents a gallon; now it’s $3.99. Tolls on some roads are now more than $100 for truckers. There are anti-terrorism identity cards and stricter emissions requirements, and any traffic infraction could send his insurance through the roof.

That’s a great deal for the trucking companies. Unlike employees, owner-operators aren’t entitled to benefits like workers compensation, Social Security contributions, unemployment insurance or the same level of protection by safety and health regulation. And it’s not just the trucking industry: Contractors have emerged all over the economy, from cheerleaders to construction workers.

The White House Takes On College Rape, Ctd

Rachel Cohen questions why the national conversation has come to focus specifically on college campuses:

There is an indisputable and often cyclical connection between poverty and sexual violence. The Bureau of Justice Statistics found that individuals with household incomes under $7,500 are twice as likely as those in the general population to become victims of sexual assault. Ninety-two percent of homeless mothers experience severe physical and/or sexual assault at some point in their lives. Sexual assault is hardly a problem limited to university campuses.

Twenty percent of college women being sexually assaulted is unacceptable. But other groups are at even greater risk. Immigrants, refugees, migrants, those suffering from addictions, minorities, LGBTQ individuals, sex workers, prisoners, the homeless, and the impoverished all experience high rates of sexual assault. And, unlike college students, these groups very often lack the knowledge, credibility, resources, and federal protections to do anything about their attacks.

And Hanna Rosin doesn’t want the conversation to ignore male victims:

Last year the National Crime Victimization Survey turned up a remarkable statistic. In asking 40,000 households about rape and sexual violence, the survey uncovered that 38 percent of incidents were against men.

The number seemed so high that it prompted researcher Lara Stemple to call the Bureau of Justice Statistics to see if it maybe it had made a mistake, or changed its terminology. After all, in years past men had accounted for somewhere between 5 and 14 percent of rape and sexual violence victims. But no, it wasn’t a mistake, officials told her, although they couldn’t explain the rise beyond guessing that maybe it had something to do with the publicity surrounding former football coach Jerry Sandusky and the Penn State sex abuse scandal. Stemple, who works with the Health and Human Rights Project at UCLA, had often wondered whether incidents of sexual violence against men were under-reported. …

So why are men suddenly showing up as victims? Every comedian has a prison rape joke and prosecutions of sexual crimes against men are still rare. But gender norms are shaking loose in a way that allows men to identify themselves—if the survey is sensitive and specific enough—as vulnerable. A recent analysis of BJS data, for example, turned up that 46 percent of male victims reported a female perpetrator.

The final outrage in Stemple and Meyer’s paper involves inmates, who aren’t counted in the general statistics at all.