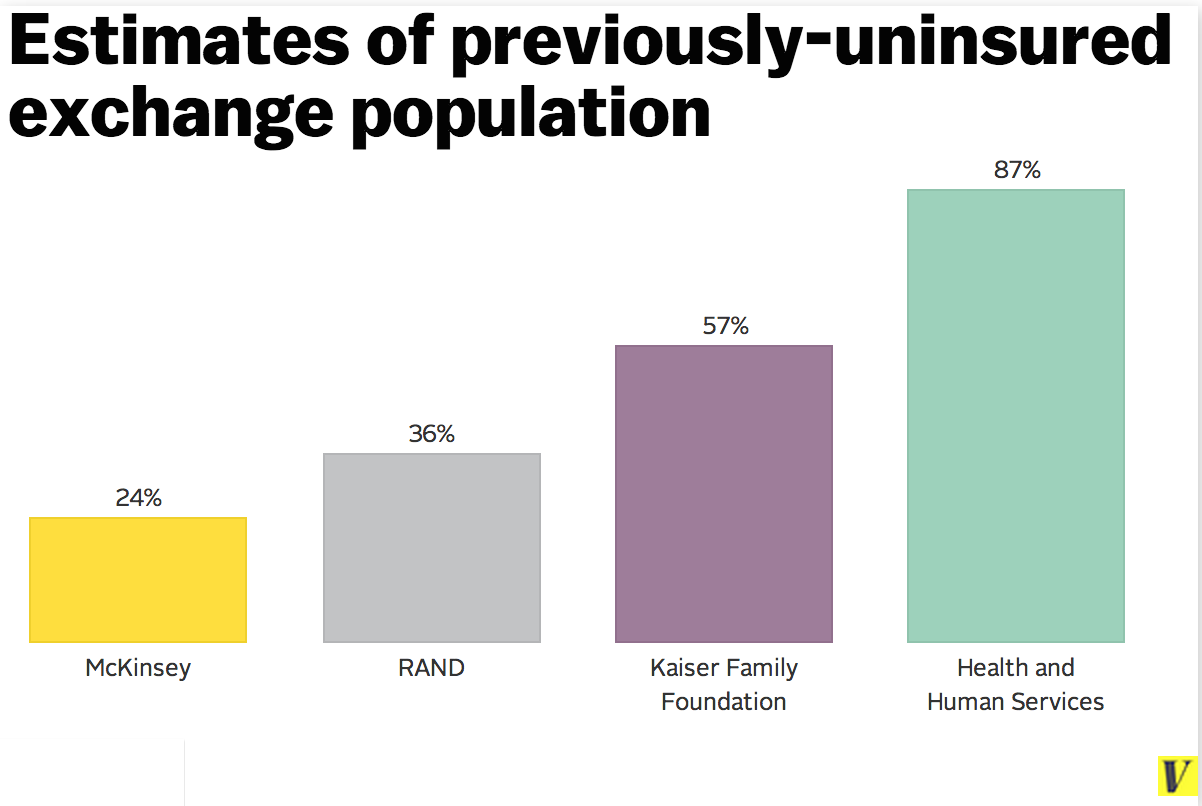

Sarah Kliff passes along the finding, from a new Kaiser survey, that a “slim majority of Obamacare’s private insurance enrollees were uninsured when they signed up for coverage.” But other organizations have produced strikingly different results:

Here’s the thing that’s so frustrating in trying to sort out this question about who was uninsured: the variation between different groups’ estimates is just massive. When you dig into the methodology, as health wonks are wont to do, you start to notice that the surveys happened at different times, with different people who were asked different questions. …

The new Kaiser Family Foundation survey is the most up-to-date, randomized study that specifically asks people to identify what coverage source they had prior to signing up on the exchange. This separates it from RAND (whose survey data misses the end of open enrollment), McKinsey (which asks a slightly different question) and the Obama administration estimate (it leaves out anyone buying through a state exchange).

Drum examines the surveys’ methodologies:

The basic problem is that the pool of uninsured has a lot of churn: people are covered for a while, then lose their jobs, then get another job, etc. So if you had insurance last August, but lost your job and signed up for Obamacare in November, do you count as previously uninsured? According to McKinsey, no. According to Kaiser, yes.

My own guess is that the Kaiser methodology is probably the closest of the four to what we’d normally think of as “uninsured,” and its sample size is big enough to be reliable.

Cohn focuses on another aspect of the survey – premium costs:

Strictly among people who had coverage previously, the “winners” (people who say they paying less for insurance now) outnumber the “losers” (people who say they are paying more for insurance now). Specifically, 46 percent of respondents who had insurance before Obamacare said they were spending less on their new monthly premiums, while 39 percent said they were spending more. That’s not much of a difference, given the survey’s margin of error. But it certainly doesn’t suggest, as the law’s opponents frequently claim, that most people are worse off. And when you consider that many people who were buying insurance on their own previously are now getting Medicaid, which is basically free, it would appear that there are clearly more winners than losers, at least when it comes to what people are paying up front for coverage.

Adrianna McIntyre expects premiums will go up next year but at a lower rate than before:

The people who enroll in health insurance in future years are expected to be healthier than the people enrolled today. The penalty for not carrying insurance is modest this year: $95 or 1 percent of income for an individual, whichever’s higher. That gets scaled up over the next few years, compelling more people to purchase insurance.

The people who declined to sign up for insurance — and pay the penalty instead — are probably healthy; had they been uninsured and sick, they would have taken advantage of new coverage options under Obamacare. As these healthier people enroll in coverage, the average health of the insured population gets better, and insurance gets cheaper.

Recent Dish on Obamacare’s costs here.