They’re going up:

The Obama administration on Friday unveiled data showing that many Americans with health insurance bought under the Affordable Care Act could face substantial price increases next year — in some cases as much as 20 percent — unless they switch plans.

Sprung calls a foul:

Unless they switch plans is the key. For the 85% of buyer who qualify for federal subsidies, their costs will not go up at all if they buy the benchmark second-cheapest Silver-level plan, or a cheaper plan — except insofar as their income rises. Their share of the premium is a fixed percentage of their income. In fact, if their income is flat they may qualify for higher Cost Sharing Reduction (CSR) benefits, since the formula for determining those benefits is adjusted yearly for inflation.

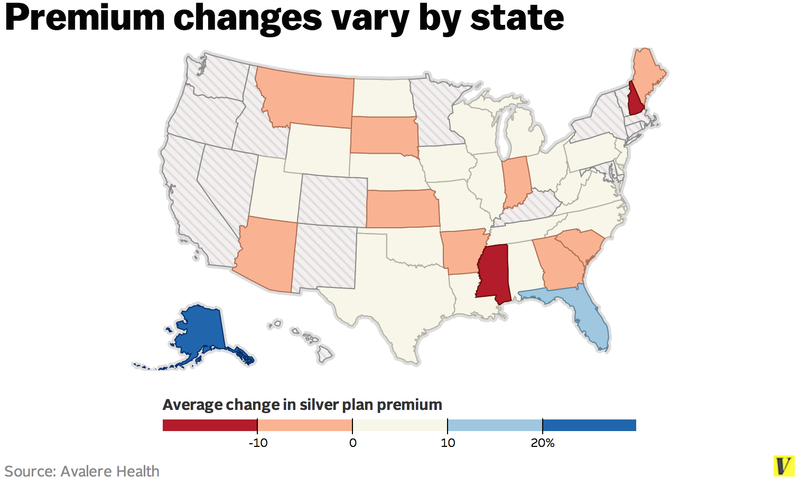

Sarah Kliff, who passes along the above map, adds that premiums “on Healthcare.gov will increase slightly in 2015 — but vary a lot depending on where you live”:

A new analysis from health research firm Avalere Health showed that, on average, premiums for bronze plans (the skimpiest products) will go up by 4 percent next year. Silver plans (which offer middle-of-the-road coverage) will have a 3 percent premium increase.

But those averages mask huge variation. Average silver premiums are falling by 18 percent in New Hampshire — but increasing 28 percent in Alaska. There are two states where average premiums are going up by more than 10 percent (Alaska and Florida) and two where they’re dropping by double digits (Mississippi and New Hampshire).

And even these state figures likely mask a lot of local variation, with premium changes likely varying from city to city.

Samger-Katz examines other research on Obamacare premiums:

The studies suggest that, in large cities, at least, the new health insurance marketplaces are working as intended: Health insurers, competing for business, are keeping prices low. That’s great news for the federal budget, since the government is paying subsidies to help some 85 percent of people on the market pay their bills. It’s also good for consumers who will be coming to the market for the first time during open enrollment, which begins Saturday.

But just because the type of plan that the researchers examined — the second-cheapest plan in the “silver” category — is showing modest changes, that doesn’t mean that every plan is a great deal. The Wakely analysis highlighted that many of the most popular plans from 2014 are getting much more expensive, while many of the cheapest plans will be new to the market in 2015. That means that consumers who simply renew their plans without shopping could get stuck with a substantial increase.

Drum encourages Obamacare enrollees to shop around:

Even if you can navigate the website yourself, be careful. Not everything is obvious at first glance. And if you’re not comfortable doing it by yourself, don’t. Get help from an expert in your state. You have three months to sign up, so there’s no rush.