According (pdf) to the CBO – in a truly dramatic turn-around. Barro throws some cold water:

This is great news about this year. But it doesn’t say very much about the long-term fiscal outlook. CBO’s revisions cut this year’s deficit by 1.3 percent of GDP, but they only shrink the next 10 years’ projected deficits by 0.3 percent of GDP.

That’s because the main factors cutting this year’s deficit are one-time effects. Half of this year’s deficit reduction comes from Fannie Mae and Freddie Mac, the mortgage giants that have been under federal conservatorship since 2008. They will make unexpectedly large dividend payments to the government this year, but that won’t happen again. The other half of this year’s change comes from higher-than-expected revenues, which are also mostly a one-time spike.

That’s a teensy bit too much cold water when you see the impact of growth on government revenues which underlies some of the data (growth that would not have happened if the GOP had adopted the premature austerity measures favored in Europe). What all this says to me is that we have a breathing space to move on longer-term spending, i.e. entitlements and defense. My own view is that Republicans are throwing away the chance of a lifetime to get a Democratic president to sign off on real entitlement reform. That would give them more cover for unpopular cuts than they will ever have if they get back into the White House. John Harwood has an excellent summary of the incentives here. Derek Thompson focuses on healthcare spending:

Here’s the story I wish more people would talk about: Our incredible shrinking Medicare projections. Since August, CBO has now revised down its projections of mandatory health care spending by nearly $500 billion, as Michael Linden pointed out. Since the 2010 CBO report, projected Medicare spending between 2013 and 2020 has fallen by just over $1 trillion … or 16%.

Among Ezra’s takeaways:

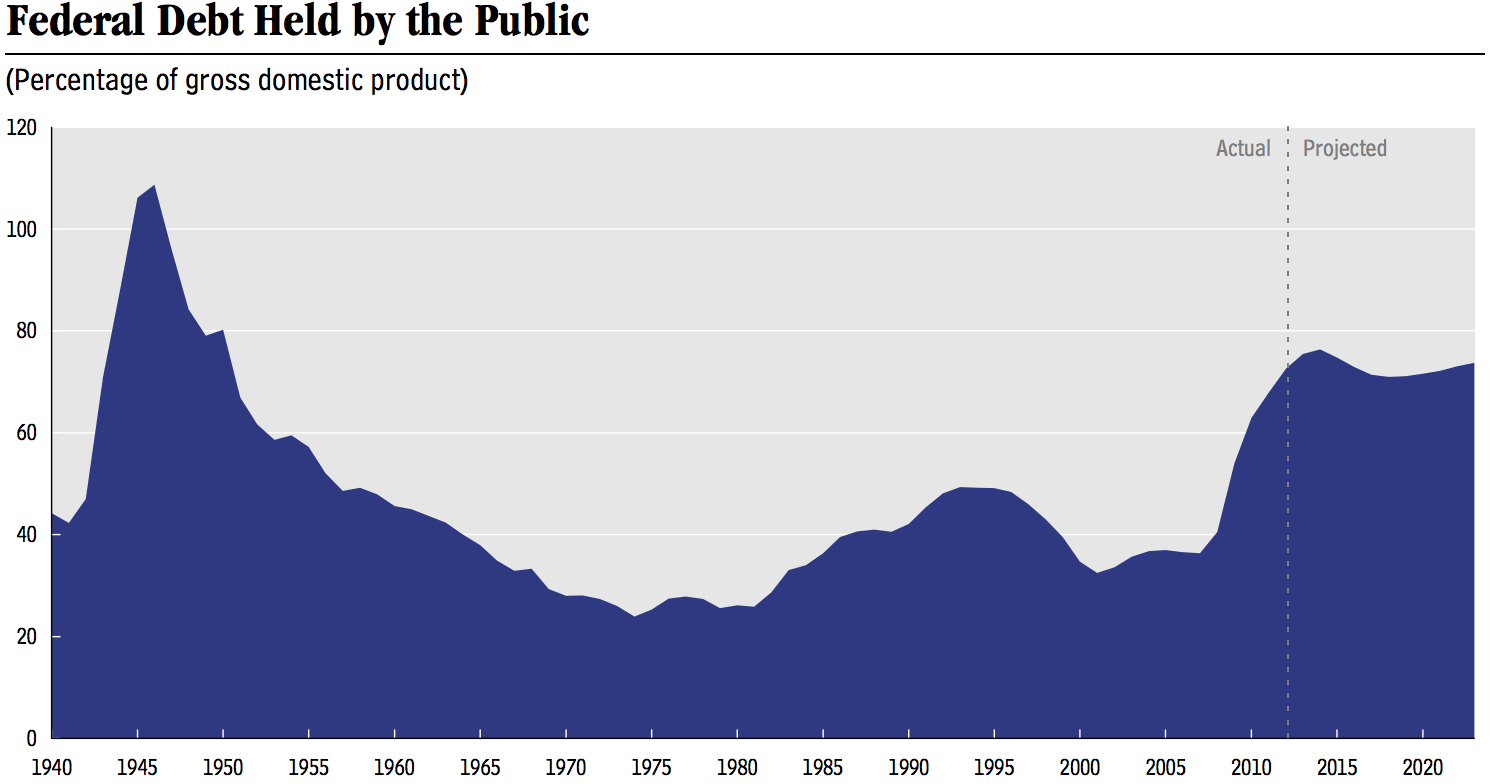

If this report clarifies anything it’s that our debt problem, insofar as we have one, is a long-term problem, not a short-term problem.

But sequestration disappears in 10 years. The policies in a deficit deal, by contrast, continue to grow. If you care about the long-term debt you should see a world in which sequestration replaces a debt deal to be a disaster. The calm of the Republican Party on this point either bespeaks a disinterest in debt or a misunderstanding about sequestration.

And Yglesias thinks long-term:

The current projection has the deficit shrinking for the next couple of years and then growing again. That leaves us with a very manageable 2024 deficit. The problem is that it’s trending upward. And nothing in this revised projection changes that fact. Under current law, the deficit will bottom out in a few years and then grow and grow forever. The flipside, though, is that there’s really no need to panic or think that there has to be a grand bargain. What we need are more measures to reduce the cost of health care and more measures to boost economic growth.