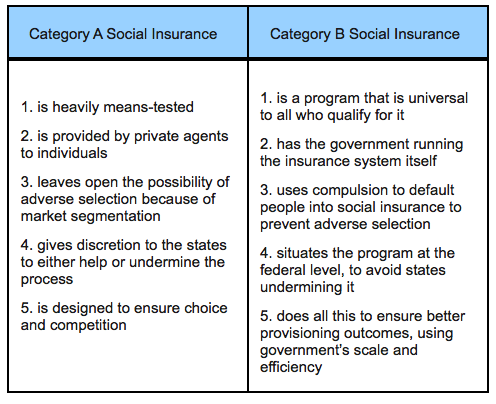

Mike Konczal blames Obamacare’s technical problems on the law’s design. He contrasts Obamacare’s form of social insurance, which he labels “Category A,” with previous forms of social insurance, such as Medicare and Social Security, which he labels “Category B”:

What we often refer to as Category A can be viewed as a “neoliberal” approach to social insurance, heavy on

private provisioning and means-testing. This term often obscures more than it helps, but think of it as a plan for reworking the entire logic of government to simply act as an enabler to market activities, with perhaps some coordinated charity to individuals most in need.

This contrasts with the Category B grouping, which we associate with the New Deal and the Great Society. This approach creates a universal floor so that individuals don’t experience basic welfare goods as commodities to buy and sell themselves. This is a continuum rather than a hard line, of course, but readers will note that Social Security and Medicare are more in Category B category rather than Category A. My man Franklin Delano Roosevelt may not have known about JavaScript and agile programming, but he knew a few things about the public provisioning of social insurance, and he realized the second category, while conceptually more work for the government, can eliminate a lot of unnecessary administrative problems.

Drum pushes back:

If I had my way, we’d have a fairly simple, universal, single-payer health care system in the United States. It would work better; provide broader coverage; and probably be cheaper than what we have now. But countries like Switzerland and the Netherlands demonstrate that an Obamacare-like system can work reasonably well too.

Konczal is certainly right to mock conservatives who don’t seem to understand that Obamacare is fundamentally a pretty conservative design for national health care—which means that if it fails, it will hardly be a failure of old-school liberalism—but I think he goes too far when he tries to blame the rollout problems on that design. There was never any realistic hope of wiping out the entire private insurance industry and instituting a single-payer system anyway, which makes this all a bit academic, but even if Obamacare is a second-best design, it’s still one that other countries have shown can be implemented effectively. I imagine that, over time, the same will be true here.

Douthat complicates Konczal’s argument:

If the Obamacare exchanges are a mess and the individual market is facing cost spirals, then conservatives are going to face some understandable skepticism (more even than usual!) from voters if they talk up the virtues of free market health care and the individual marketplace in 2016 and beyond. But in principle, the distinction between Obamacare’s approach to health policy and the conservative version of means-testing, block-granting, and competitive marketplaces is clear enough. That’s because while Obamacare may be using neoliberal rather than New Deal-style means, it’s still chasing essentially left-of-center ends: It seeks a level of universality and comprehensiveness that conservatives don’t think is necessarily worth pursuing. And it’s that quest, those goals, that require the complicated mandate-regulate-subsidize combination that could undo the individual marketplace if the enrollment isn’t where it needs to be and the subsidies and fines and regulations aren’t successfully fine-tuned.

In other words, pace Konczal, the potential problems with Obamacare aren’t necessarily “driven by means-testing, state-level decisions and privatization of social insurance.” They’re driven by the law’s attempt to employ these (notionally) decentralized means while still seeking essentially centralized ends.

Reihan thinks health reform should have had a default option:

The idea of a default option comes to mind in light of the difficulties facing the new health insurance exchanges. Even in the absence of technical difficulties, I’m starting to wonder why anyone thought that a substantial majority of healthy young people would sign up for coverage, including heavily subsidized coverage. The threat of a penalty is one obvious reason. Yet the Obama administration and its allies have been reluctant to emphasize the punitive dimension of the individual mandate, for obvious political reasons. Rather than using the threat of a penalty to spur enrollment, coverage expansion advocates have emphasized the benefits of insurance, hence the (apparent) reluctance of the architects of the exchanges to expose consumers to the full, unsubsidized cost of the new insurance options.