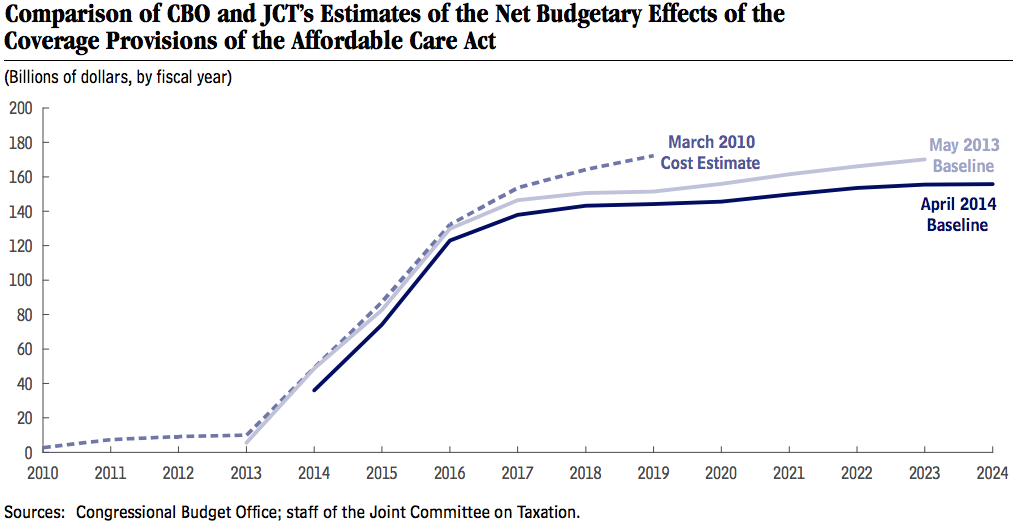

Yesterday, the CBO estimated (pdf) that the ACA will be cheaper than originally projected:

Cohn explains why costs have decreased:

The higher the premiums, the more expensive the subsidies. And that’s where the law has, so far, outperformed expectations. Insurers are offering plans with lower premiums than CBO and other experts had predicted. As a result, the federal government is on the hook for less financial assistance.

Better still, the CBO says that it doesn’t expect across-the-board premium spikes next year, as the law’s critics and even some insurance company officials have speculated would happen. Of course, the CBO could be totally wrong about that. And even if it’s not wrong about what’s likely to happen to premiums overall, it’s possible—I’d say likely—that prices in some parts of the country will go up significantly next year. But CBO’s new projections would put such rate increases into better, more favorable perspective. Premiums are already lower than expected. The law is already reducing the deficit by more than expected. So even if premiums rise next year or beyond, the law could still end up calling for lower spending—and more deficit reduction—than the original projections suggested.

Drum makes an important counterpoint:

The bad news: the lower cost of premiums is primarily because the quality of the plans coming from insurers is lower than CBO originally estimated: “The plans being offered through exchanges in 2014 appear to have, in general, lower payment rates for providers, narrower networks of providers, and tighter management of their subscribers’ use of health care than employment-based plans do. Those features allow insurers that offer plans through the exchanges to charge lower premiums (although they also make plans somewhat less attractive to potential enrollees).”

McArdle weighs in:

The good news is that [shrinking provider networks] keeps premiums low. The bad news is that, over time, the CBO doesn’t think this will be sustainable. As more people exit the employer-based market for the exchanges, insurers will have to broaden their networks; they just can’t serve that number of customers with the networks they have, and if they try to keep the networks small, regulators will probably have something to say.

It’s worth noting, as I always do, that the CBO is required to assume that the current law will go into effect: that the employer mandate and the individual mandate are enforced, all the delayed provisions are allowed to take effect, the grandfathering ends. It’s also worth noting, as I always do, that the CBO does not have a crystal ball: We’ve never done anything like this before, so it is necessarily trying to reason from situations that aren’t necessarily great analogies for what we’re doing now. This is no slam on the office; it’s doing the best it can. But its projections may differ significantly from what actually happens.