Jared Bernstein reacts to the new Commerce report:

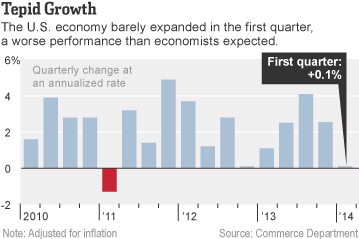

[R]eal GDP grew only 0.1% in the first quarter of the year, according to this morning’s report from the Commerce Dept. That’s a huge deceleration from last quarter’s 2.6%, and well below analysts expectations of around 1.2%.

Remember, that 0.1% is an annualized number–the actual, quarterly percent growth of GDP was 0.03%, meaning that the real level of the value of goods and services in the US economy was essentially unchanged in the first three months of the year. That’s unusual and alarming, if it’s correct.

However, given the jumpiness in the quarterly estimates, and this is the first of three estimates, based on preliminary data, it’s important to look at year-over-year results as well, to smooth out some noise, including recent weather effects. By that measure, real GDP is up 2.3%, a deceleration from last quarter’s 2.6%. In that regard, look at this quarter’s number as a stern warning, one that may or may not herald a downshift in GDP growth, but one that is hopefully not indicative of the underlying trend.

Neil Irwin digs into the data:

Business investment … contributed quite a lot to growth from 2011 to 2013, as companies increased their investments. Companies have been adding buildings, buying new equipment and acquiring new software packages strongly enough that such investment contributed 0.84 percentage points to growth in 2011, almost precisely the same as in 2012. The contribution shifted down to a third of a percentage point in 2013.

In the first quarter of 2014, however, the corporate sector was a net negative for the economy, with investment in structures, equipment and intellectual property falling at a 2.1 percent annual rate, enough to subtract a quarter of a percentage point from overall G.D.P. That was surely in part caused by the harsh winter weather, but the basic trend is real: American business, once a major driver of the expansion, no longer is.

Ben Casselman adds an important caveat:

A key note of caution: Preliminary GDP estimates are notoriously unreliable. On average, the figures get revised by half a percentage point between the first and second estimate (which we’ll get next month) and by a whopping 1.3 percentage points when the final numbers come in.

Jordan Weissmann chimes in:

Most economists seem ready to chalk up much of the slowdown to the miserable winter weather, which kept shoppers indoors, slowed construction, and otherwise turned the last few months into a cold and soggy mess. Chances are, there will be some rebound this quarter—a spring awakening, if you will.

Still, one part of the report seems like a genuine cause for concern: housing.Residential investment has now fallen for two straight quarters.

James Pethokoukis’s view:

How does the economy typically respond after a weak, but positive GDP quarter? It varies. After that weak 4Q 2012, GDP growth averaged 1.8% over the next two quarters. After 0.3% growth in 1Q 2007, growth averaged 2.9% over the next six months. A 0.2% 4Q 2002 was also followed by 2.9% growth the subsequent two quarters. Then again, weak quarters in late 1990 and 2000 were quickly followed by recessions within six months. This time around, however, odds are growth will accelerate — weather permitting.

(Chart via the WSJ)