Derek Thompson fingers “invisible unemployment”:

What is “invisible unemployment”? It’s discouraged workers and part-timers who want more hours. The official unemployment rate doesn’t consider them unemployed. So when we talk about the official unemployment rate—now at a lowish 5.8 percent—we’re ignoring these workers. They’re statistically invisible. Here’s a picture of invisible unemployment (in blue) vs. official unemployment (in red). Since early 2010, the number of unemployed Americans has declined by twice as fast as the number of discouraged/part-timers (42 percent vs. 21 percent).

In 2002, official unemployment swamped invisible unemployment. The official unemployment rate was an accurate description of the labor force. But the spread between invisible and official unemployment is shrinking. In the last 20 years, the six months with the smallest gaps between official and invisible unemployment were all in 2014. That means the official unemployment rate is getting worse and worse at describing the real conditions facing American workers.

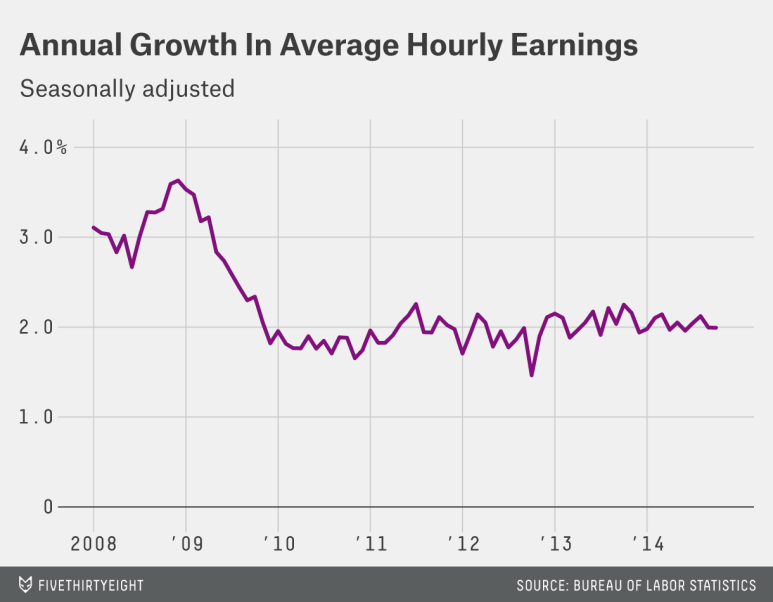

Ben Casselman focuses on our weak wage growth:

The average worker earned $24.57 an hour in October, up 2 percent from a year earlier. Even as hiring has picked up and unemployment has fallen, wages growth has remained decidedly anemic.

From an economics perspective, modest wage growth isn’t an entirely bad thing. It suggests that employers aren’t struggling to find workers to fill the available jobs, which means employment growth can continue without the economy overheating. For policymakers at the Federal Reserve, it means they can keep trying to boost the economy with low interest rates without worrying too much about inflation.

But for workers, the earnings figures mean that they aren’t seeing the economic recovery reflected in their paychecks. Until that changes, they’re unlikely to take much comfort in jobs-day headlines, no matter how positive.

Greg Ip adds that “productivity is up only 0.9% in the last year, lower than the 1.3% average recorded since the recession, itself none too impressive”:

Both weak pay and productivity might be related to the sorts of jobs growing the most; Steve Blitz of ITG reckons almost 70% of this month’s private sector job growth were in temporary work, health care and restaurants. Manufacturing and construction both rose, but by slim numbers.

But Weissmann remarks that “some, like Moody’s Analytics economist Mark Zandi, are convinced wage spikes are just around the corner”:

Even though the overall unemployment rate is still high by long-term standards, some analysts believe that the millions of the long-term jobless are essentially unhireable—meaning that employers are actually looking at a much smaller labor pool. The short-term unemployment rate is already almost back to normal, and to them, that indicates pay raises are on the way. If they are, we can only hope that the Fed doesn’t overreact and throw cold water on the economy before it ever really gets hot.