Patrick J. Egan puts the premium hikes in perspective:

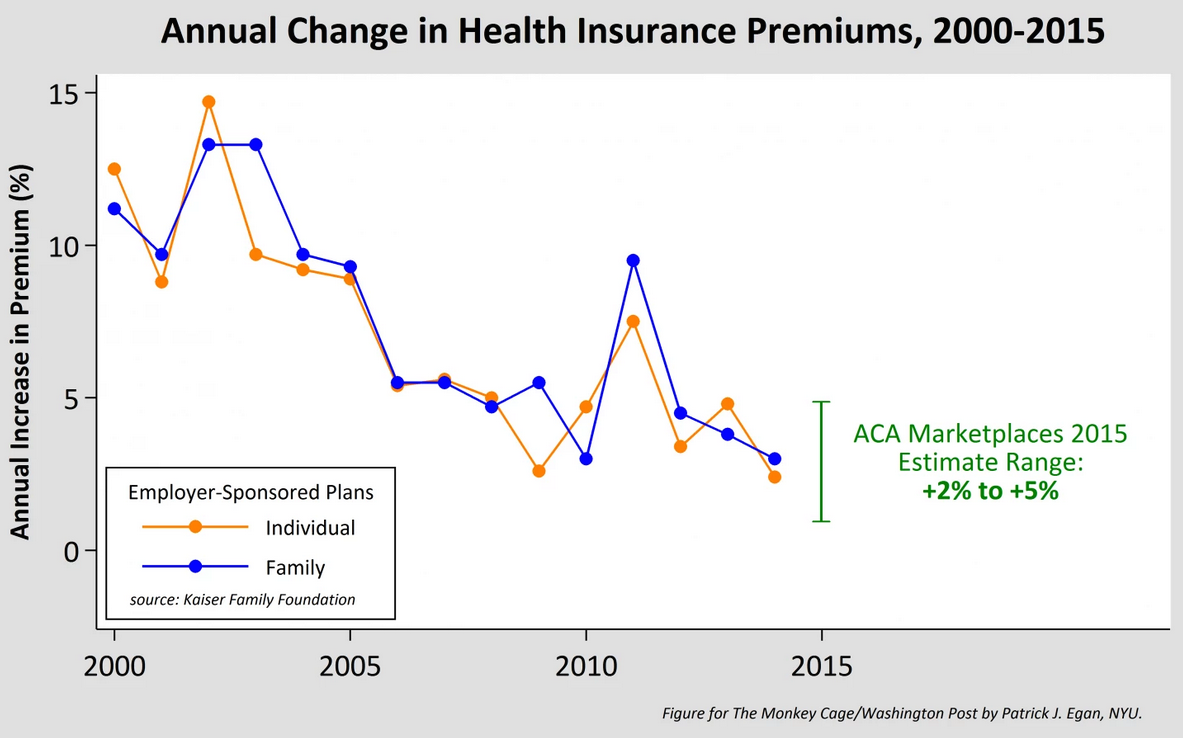

ACA premiums are rising. But most reporting on these numbers has lacked a critical bit of historical context. These price increases are no higher than recent premium increases on plans provided to Americans by their employers. Since 1999, the Kaiser Family Foundation has interviewed a nationally representative sample of employers about the health insurance they offer. The graph above displays changes in the average annual premiums paid for single and family coverage since 2000. Before 2007, increases were at least 5 percent per year. Since then, premiums have been rising more slowly, with the median increase at about 4 percent per year. Shown alongside these figures is the range of estimates published over the past few days on expected premium increases on plans in the ACA marketplaces. They’re no different from recent trends in premiums for employer-sponsored plans.

Some Americans may need to “shop around” for a “better deal” (as HHS officials are putting it) — particularly those who face a price increase from their current insurer. But here again, context is helpful. More than half of the firms in the Kaiser Family Foundation survey reported doing the same thing last year: 58 percent said they shopped for a new plan or a new insurer, and 27 percent of those who shopped changed carriers.

Jonathan Cohn chimes in:

Health insurance premiums go up almost every year, just because of inflation and ever-improving technology, so modest hikes like these are good news. Even better news is the fact that, in some markets, the price of the benchmark silver plan has actually declined—something that almost never happens health care. As Larry Levitt, senior vice president of the Kaiser Family Foundation, observed earlier this year when such changes first became apparent, that’s like “defying the laws of physics.”

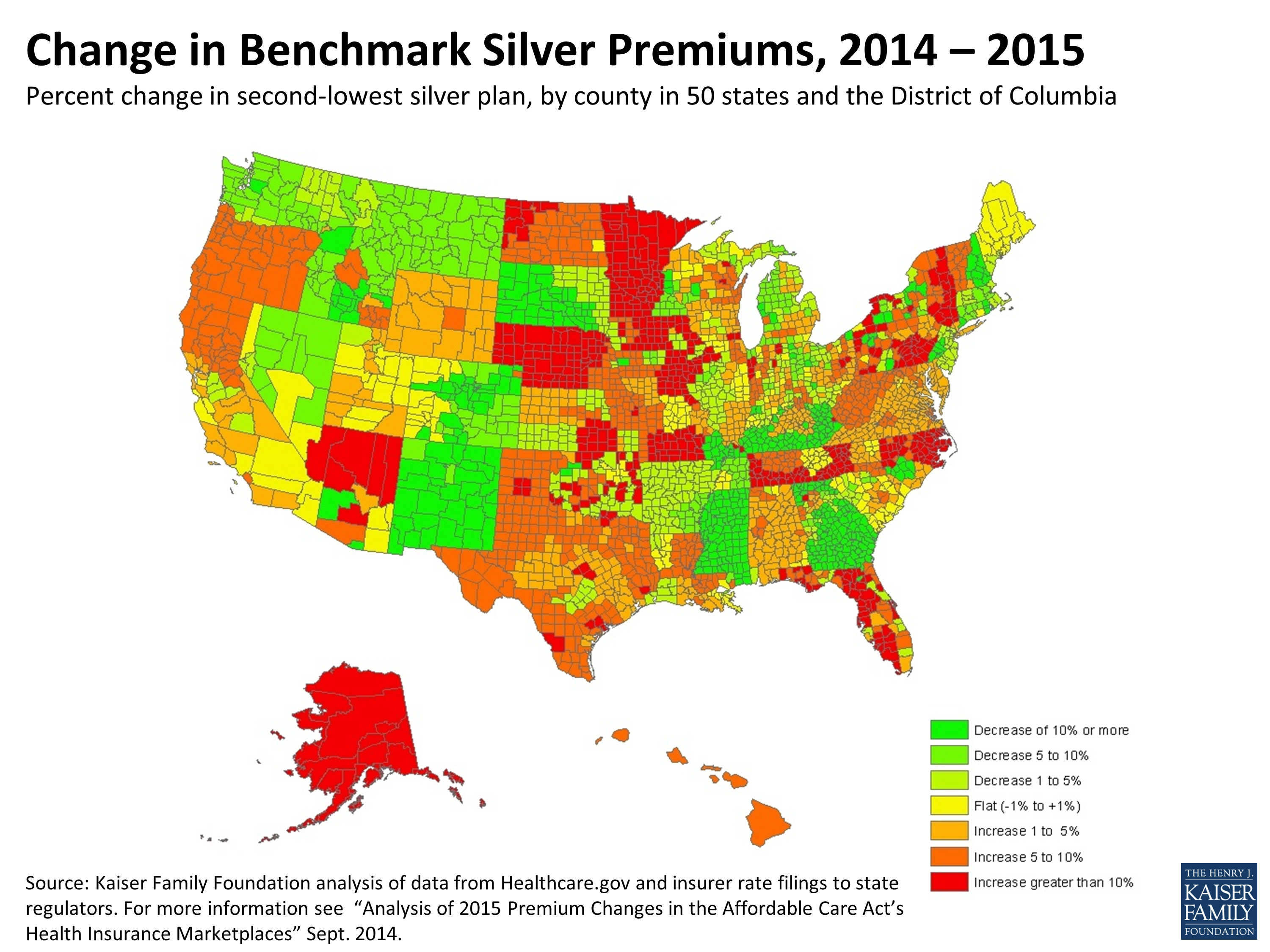

So what’s not to like? Well, these trends and averages mask tons of variation. New insurers are jumping into the marketplaces and in many cases they are offering newer, cheaper options. In addition, some insurers who last year asked for high premiums have decided to lower their prices. The common goal of both is to attract more customers and, all else equal, it’s a sign that the markets are healthy. But some insurers are raising prices, because they underestimated costs last year. Here’s what the prices look like, across the country: