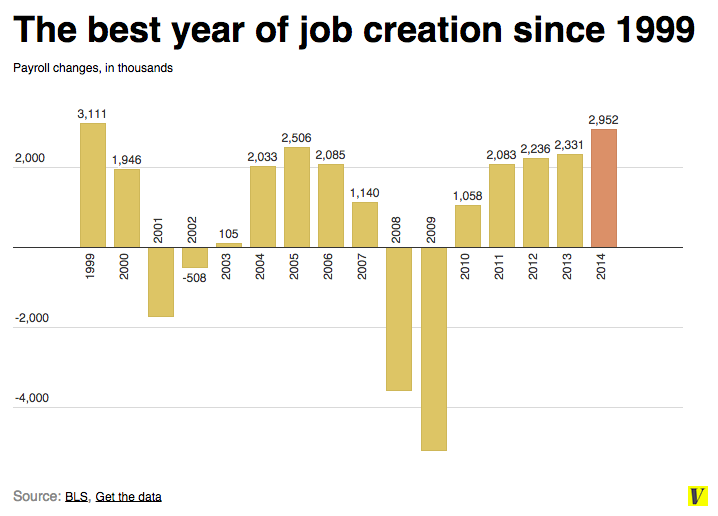

Danielle Kurtzleben illustrates the ones we added last year:

Chait expects this to transform politics:

The recovery is not complete — wages remain stubbornly suppressed — but this fact itself suggests an upside: The absence of higher pay is also the absence of any kind of inflationary pressure that might cause the Federal Reserve to apply the brakes to the recovery. This in turn suggests job growth is not finished. The 2016 elections could well take place against a backdrop of full employment. The entire predicate of the Republican argument since 2009 — that Obama’s massive expansion of spending, taxes, and regulation has snuffed out job creators’ incentive or ability to work their capitalistic magic — will be moot.

In 1996, the recovery was still embryonic enough that Bob Dole could lamely assert that Americans were suffering from “the Clinton crunch.” Four years later, George W. Bush had to acknowledge widespread prosperity, while casting himself as the ideological heir to Clinton’s moderate policies and running on “honor and dignity.” That is the sort of reversal currently under way.

Ben Casselman is more cautious:

It’s possible that the economy is poised for a breakout in 2015 and we just don’t know it. Average wages are a blunt measure, lumping together everyone from CEOs to fast-food workers, so it can be hard to pick up trends bubbling beneath the surface. There are at least a few individual sectors in which earnings are rising faster.

But after five years of dashed expectations, it’s probably wise to stay in a “show me” mind-set. The economy finally showed us job growth in 2014. For wages, though, we’ll have to wait to see what 2015 reveals.

Pethokoukis throws some cold water:

Some analysts think the next 12 months will show a big step-up in GDP and earnings growth, thanks in no small part to the 50% drop in oil prices. Citi just raised its projection for GDP growth by ½ percentage point to a robust 3.6% for 2015. We’ll see. As BTIG strategist Dan Green puts it, “The simple fact is we cannot consider an employment report a success, no matter how healthy the headline may be, if wage data does not begin to accelerate.”

Bloomberg View’s editors speculate that, “to some extent, the decline in global oil prices may be holding U.S. wages down”:

The average wage in mining and logging, a category that includes oil extraction, has fallen at an annualized rate of almost 5 percent during the past three months.

But McArdle sees the low oil prices as a major economic stimulus:

In 2009, economist James Hamilton suggested that most of the GDP loss in the Great Recession could be explained by looking at the very high price of oil that preceded it. A more recent paper from the Fed assigns a lesser role, but still a significant one. The current confluence of strengthening jobs numbers and falling oil prices may suggest that they are right–not that jobs and GDP will fluctuate month to month along with the price of oil, but that positive and negative price shocks may also produce correspondingly positive and negative effects on our economy.

Neil Irwin digs further into the report:

One mild curiosity in the report is that the size of the labor force actually fell, with 273,000 people no longer either holding a job or looking for one. That may be a statistical aberration, but even over a longer period of time the steep drop in the labor force since 2008 has not reversed itself. It’s partly demographic, with more baby boomers nearing retirement age. But the wage numbers also suggest another reason: When employers are so reluctant to raise pay, it shouldn’t be shocking that more Americans choose to sit at home and remain out of the labor force.

Drum looks at the big picture:

Overall, this jobs report is decent news, but hardly great. Until we start to see steady employment growth and steady wage growth, the labor market still has a lot of slack no matter what the headline unemployment rate is. Given this, in addition to possible headwinds in the rest of the world, the Fed needs to continue to keep interest rates low for quite a while longer. It’s not yet time to tighten.