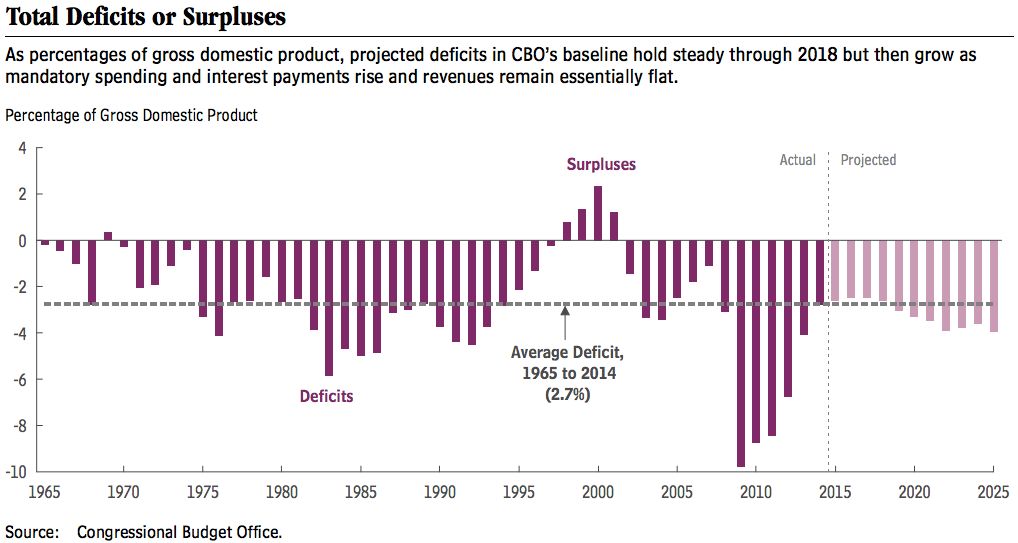

Deficits are predicted to rise somewhat in the near future:

The U.S. deficit will fall to its lowest level since 2007, but it is expected to begin rising quickly after 2018, according to a new report from the Congressional Budget Office. The difference between federal spending and revenue will fall to $468 billion or 2.6% of GDP this fiscal year, which is the lowest level since 2007, the CBO says. The deficit will continue to fall slightly in 2016 and hold steady in 2017. But then it will begin rising once more, reaching 3.0% of GDP in 2019 and 4.0% in 2025.

Matt Klein looks at the causes of those larger deficits:

More than all of the projected increase in the US federal budget deficit between now and 2025 is expected to come from higher interest payments on the existing debt.

He goes on to wonder whether those larger deficits will materialize. Krugman seconds Klein:

CBO shows the ratio of debt to GDP barely rising; just about all the rise in payments comes from an assumption that interest rates will rise. And as both Klein and I have tried to explain, we don’t really know that; there’s a plausible case that it’s wrong.

I’m not attacking CBO, which needs to make some kind of rate assumption. But if you read someone trying to resurrect deficit panic, bear in mind that even the modest rise in the new projections is just an assumption, with nothing solid behind it.

focuses on the uncertainty of Medicare spending. She questions the continuation of the “phenomenally slow growth in Medicare spending in recent years”:

Though some of this slowdown is well understood—reflecting payment cuts under the Affordable Care Act and the expiration of patents of a number of blockbuster drugs—much of the slowdown in Medicare spending is not understood by analysts. CBO’s research suggests that the Medicare slowdown does not appear to be attributable to the recession, and my work, using a variety of data sources, concurs.

CBO has made the not-unreasonable assumption that this slowdown will persist for some time. But, because we don’t understand why Medicare spending has slowed, this assumption must be viewed as highly uncertain. It is possible that, rather than persisting, the slowdown could reverse itself, and spending growth could surprise us on the upside in coming years.

Josh Zumbrun pays attention to the growth estimates:

These small deficits may seem surprising given the ferocity of Congress’s recent budget battles. But perhaps even more noteworthy is the economic forecast underlying it. The CBO currently estimates the recovery will continue through at least the end of 2017. If correct, that will be a 102-month economic recovery: the third-longest in U.S. history. The CBO’s forecasts for growth are not that different from the Federal Reserve’s, where policy makers also forecast at least three more years of economic expansion.

Finally, William Gale keeps in mind that the Great Recession pushed “public debt to all-time peace-time highs relative to the size of the economy”:

The debt-GDP ratio stands at 74 percent currently, up from an average of 37 percent in 1957-2007, the 50 years before the Great Recession, and a value of 35 percent as of 2007. The only time in U.S. history that the debt-GDP ratio has been higher is during and just after World War II, when the massive mobilization effort raised debt to more than 100 percent of GDP. …

The current high level of debt is not a crisis by any means. We are not Greece or even close. We do not need immediate cuts in spending or tax increases; indeed, they would probably be harmful to overall growth, as the economy is still in recovery mode. But the high debt level is not good news, and it is a problem to keep an eye on.