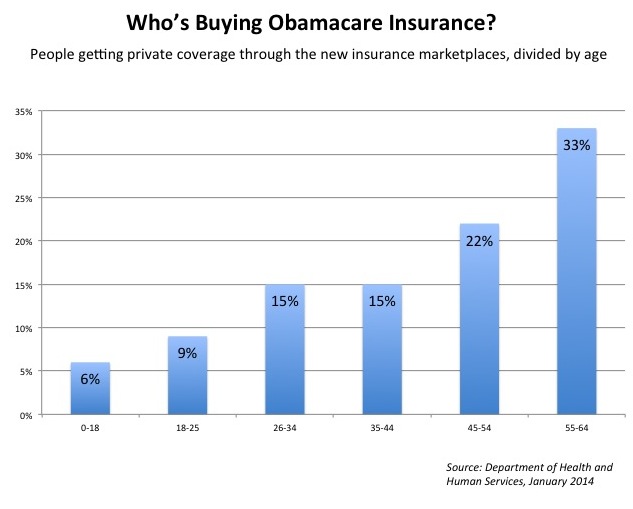

Yesterday, the government released detailed data on Obamacare enrollments. Cohn provides the chart seen above:

The figure bound to get most attention is the age breakdown. Insurers rely on premiums from healthier people to offset the costs of people with significant medical bills. And young people are a reasonably good proxy for healthy people—or, at least, as good a proxy as we have right now. According to a recent study by the Kaiser Family Foundation, about 40 percent of the population that could enroll in Obamacare exchange plans are between the ages of 18 and 34. But, according to the government’s new data, only 24 percent of the people signing up for coverage are in that age range. In short, the people who have gotten insurance through the Obamacare marketplaces so far are significantly older than the people who could, in theory, be buying insurance from them.

But is that really a big deal? In Massachusetts, according to analysis from MIT economist (and Obamacare architect) Jonathan Gruber, younger people tended to sign up later.

Philip Klein pushes back:

Though there’s a plausible case to be made that younger Americans will wait until later to sign up, the administration is still in a deep hole. Because the current number of young adult signups is significantly less than 40 percent, to make up ground, signups in the coming months will have to be significantly higher than 40 percent.

As an example, let’s just say all of the roughly 2.2 million Americans whom HHS says have signed up for insurance pay their premiums and complete enrollment, and the total paid enrollment number through March ends up being 5 million people. To meet the original demographic goal, about 1.4 million of the remaining 2.8 million enrollees — or roughly half — would have to be between the ages of 18 and 34.

Sarah Kliff digs deeper into the numbers:

Even more important than these top-line numbers is what’s happening in each state. Insurance rates are set on a state-by-state basis, so even if thousands of young people are signing up in California, it doesn’t effect the premiums in neighboring Nevada.

The new Health and Human Services report does show some variation by state, although most exchanges tend to hover somewhere in the 20-percent range. In the District of Columbia, 44 percent of enrollees are young adults, the highest for any exchange (and remember: This is just the individual marketplace, not the small business exchange where Congressional staff shop). Arizona and West Virginia have the lowest rates of young adult sign-ups, who make up 17 percent of their marketplace.

Avik Roy considers what happens if the exchanges skew older:

As Philip Klein notes, a recent article by Larry Levitt, Gary Claxton, and Anthony Damico of the Kaiser Family Foundation described an enrollment of 25 percent among 18-34 year olds as a “worst-case scenario,” estimating that insurers would lose money on these plans, because “overall costs…would be about 2.4% higher than premium revenues.” 2.4 percent may seem like a small number, but given that the average insurer has profit margins of 4 to 6 percent, a 2.4 loss on premiums—before we even count overhead costs—is a serious problem. It’s why Humana reported to the Securities and Exchange Commission that it expected meaningful losses in its exchange-based plans.

McArdle looks at the percentage of enrollees receiving subsidies:

Five million people were deemed eligible to buy a policy on the exchanges; 2.7 million, or 54 percent of them, were eligible for subsidies. But of people who actually selected a plan, 1.68 million, or 80 percent, were subsidized. To put it another way, 62 percent of the people eligible for subsidies selected a plan, but only 8.5 percent of those who weren’t eligible for subsidies actually purchased one. That is very different from the information we were getting in December, when most of the people who selected plans were not eligible for subsidies. … This is much closer to what the Congressional Budget Office was projecting, in terms of subsidized enrollment; it had predicted that about 85 percent of the people on the exchanges would get subsidies. So in one sense, it’s not novel. But it does show enrollment looking a lot more like the wonks had been projecting, and that’s important. The next step for the administration is to get the mix of young and healthy people more in line with initial forecasts.

Sprung looks on the bright side:

Signup rates are impressive in many large states in which Republican governors and legislatures have worked actively to undercut the law. On 12/28, the open enrollment period (Oct. 1 – Mar. 31) was just shy of half over — and signups were miniscule through the first week of December. Any state that had reached more than say one third of the CBO projection for first-year exchange signups might be deemed more or less on course. Major non-cooperating states that passed that threshold (as tracked by Charles Gaba’s invaluable spreadsheet)include Florida (33% of CBO projection, 158.0k signups), Michigan (47%, 75.5k), New Jersey (36%, 34.7k), North Carolina ((56%, 107.7k), Pennsylvania (39%, 81.3k), Virginia (35%, 44.6k) and Wisconsin (52%, 40.7k).

More good news: only about 20% of those choosing plans on the exchanges have opted for the cheapest bronze plans, where deductibles average $5,000 per person. Benefits are benchmarked to the second cheapest silver plan in each state, and subsidies that reduce deductibles. and maximum out-of-pocket costs, offered to buyers with incomes below 200% of the federal poverty level, are only available to silver plan buyers. Further, 79% of those who have enrolled in plans thus far have qualified for subsidies. Put those numbers together and it appears that most exchange buyers thus far may indeed find their coverage and care affordable.