Yesterday, Greece’s Prime Minister Antonis Samaras called snap elections after the parliament rejected his candidate for president a third time:

The trigger for the elections was the failure at the third and final attempt of Samaras’s bid to push through his nominee for president, Stavros Dimas. Dimas attracted the support of 168 lawmakers in the 300-seat chamber, short of the 180 votes required. Under the constitution, the legislature must now be dissolved and a date for elections set. Samaras said he’ll meet tomorrow with the incumbent president, Karolos Papoulias, and ask for the election to be held on Jan. 25. That’s just weeks before Greece’s 240 billion-euro ($293 billion) bailout expires.

Mark Gilbert explains why Greece’s political crisis could have ramifications for the entire Eurozone:

Polls suggest that the opposition Syriza party may win power in Greece; its leader, Alexis Tsipras, wants to unwind government spending cuts to halt what he calls a “humanitarian crisis” in his country. If he does win the prime minister’s job on Jan. 25, the EU will need to take his concerns seriously, recognize that fiscal backtracking is preferable to seeing Greece exit the euro, and concede that the unfortunate solution to the nation’s unsustainable debt is to forgive some of it. …

The EU’s apparatchiks will need to take seriously Syriza’s demands for an easing of Greece’s economic strictures — or risk turning the political drama into an economic crisis. If Greece were to abandon the common currency project, it would call into question the membership credentials of other euro nations. (Note that Portuguese bonds are also taking fright today.)

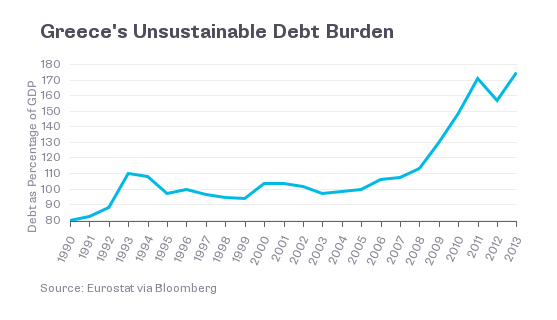

Danny Vinik also warns of a Eurozone crisis if Syriza wins:

[M]arkets are nervous. Germany has an outsized influence at both the ECB and European Commission, and is determined to use its financial leverage to force Greece to make structural changes to its economy. If Germany becomes determined to hold a hard-line negotiations with the Syriza-run Greek government, the odds of a “Grexit” could rise substantially. Already on Monday, yields on 10-year Greek bonds rose nearly 1 percentage point, to 9.7 percent. That could provoke similar fears in other periphery nations in the Eurozone.

That is all months off. Greek attitudes toward Syriza may shift if the party’s chance of gaining control of the government increases. There may be another political stalemate with parties unable to form a governing coalition. But the risks are real—not just for Europe’s economy, but the world’s.

Yglesias runs down some other possible outcomes:

One can also imagine a scenario in which parties of the far-left and far-right (including the fascist Golden Dawn) gain enough votes that no politically viable coalition is mathematically workable. In that case, well, it’s not really clear what would happen. Something along these lines occurred briefly in 2012 leading to a short-term “caretaker” government of Brussels- and Frankfurt-approved technocrats. That could happen again, or you could have the kind of more severe political crisis that sometimes occurs when a country endures a years-long spell of unemployment over 20 percent.

But Douglas Elliott downplays the potential for a Greek tragedy:

It is quite unlikely that Greece will end up falling out of the Euro system and no other outcome would have much of a contagion effect within Europe. Even if Greece did exit the Euro, there is now a strong possibility that the damage could be confined largely to Greece, since no other nation now appears likely to exit, even in a crisis.

Neither Syriza nor the Greek public (according to every poll) wants to pull out of the Euro system and they have massive economic incentives to avoid such an outcome, since the transition would almost certainly plunge Greece back into severe recession, if not outright depression. So, a withdrawal would have to be the result of a series of major miscalculations by Syriza and its European partners. This is not out of the question, but the probability is very low, since there would be multiple decision points at which the two sides could walk back from an impending exit.

Likewise, Neil Irwin sees no signs of a periphery-wide panic:

[W]hat we’re not seeing is the kind of contagion that was widespread from 2010 to 2012. At that time, any sign that the crisis was worsening in Greece immediately translated, through the financial markets, into greater panic about the much larger European economies of Spain and Italy. … But Greece’s latest troubles don’t seem to be adding much to economic and financial uncertainty beyond Greece. Spanish and Italian bond prices fell a bit Monday and their yields rose a bit, but Spain’s 10-year borrowing costs are now at 1.67 percent and Italy’s at 1.98 percent, much closer to Germany than to Greece.