The dubiously elite continental currency club admitted a new member over the holidays:

On Thursday, Lithuania became the 19th country to join the euro zone. The move made it the last Baltic nation to adopt the currency, and the timing was inauspicious—the euro looks more and more like an economic death sentence as depressions spread across the continent. Proving skeptics right, less than 24 hours later, the currency’s value dropped to a four-year low after European Central Bank President Mario Draghi seemed to suggest that the bank might start printing money to combat what he called “excessively low” inflation. The Financial Times noted that with the latest dip, the euro’s value “has fallen by 12 percent against the dollar in the past six months.”

Matt O’Brien calls Vilnius’s gambit “another reminder that the euro, which isn’t so much a currency as a doomsday device for turning recessions into depressions, has always been much more about politics than economics”:

In Lithuania’s case, those politics come down to four words: breaking free of Russia.

That, after all, sums up their last 100 years of history. … Indeed, it’s no coincidence that Lithuania’s support for joining the euro has gone from 41 percent in 2013 to 63 percent today in the wake of Russia’s incursion into Ukraine. Freedom, in other words, is worth a euro-induced depression. It’d better be, because that’s what Lithuania has gotten. It pegged its currency to the euro back in 2002, you see, so it’s been importing the euro-zone’s monetary policy for over 12 years now. And, like the other Baltics, that’s ended quite poorly for them. Lithuania went on a borrowing binge — its current account deficit reached a staggering 14 percent of GDP in 2007 — as rates that were too low for its still-catching up economy pushed housing prices if not into the stratosphere, at least into the lower level clouds.

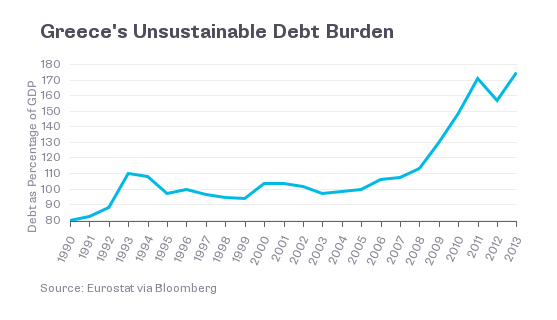

At the same time, Mike Bird notes, the chances the Greece will take the heretofore unthinkable step of exiting the euro have increased:

That’s because Syriza, the radical leftist coalition that wants to tear up the country’s bailout rules, looks likely to win [the general election on Jan. 25]. That means a game of chicken with the EU institutions and International Monetary Fund. If either side refuses to back down, there could be market chaos, bank runs, and a forced exit from the euro. … It’s not Syriza’s official policy to leave the euro, but a solid portion of the group are happy that route, and others may join them — if pushed.

The Greeks’ disillusionment with the currency stems largely from the European Central Bank’s unwillingness to take steps to boost employment in peripheral countries at the risk of increasing inflation, which Germany (the eurozone hegemon) fears. However, David R. Kotok thinks that’s about to change:

The economies of Europe are on a very flat growth path. They have high unemployment, large structural impediments, no apparent inflation, and either extraordinarily low growth or actual shrinkage, depending on which country we examine. The tool of European fiscal policy is hampered by huge deficits and lots of unfunded social liabilities.

Monetary expansion is the only game in town. Interest rates have already fallen to levels below zero in some shorter-term instruments and near zero in others. We expect a large monetary stimulus to originate from the European Central Bank as early as the end of this month. Markets are building this expectation, which will mean a huge market disappointment if the ECB does nothing.

(Chart via xe.com)